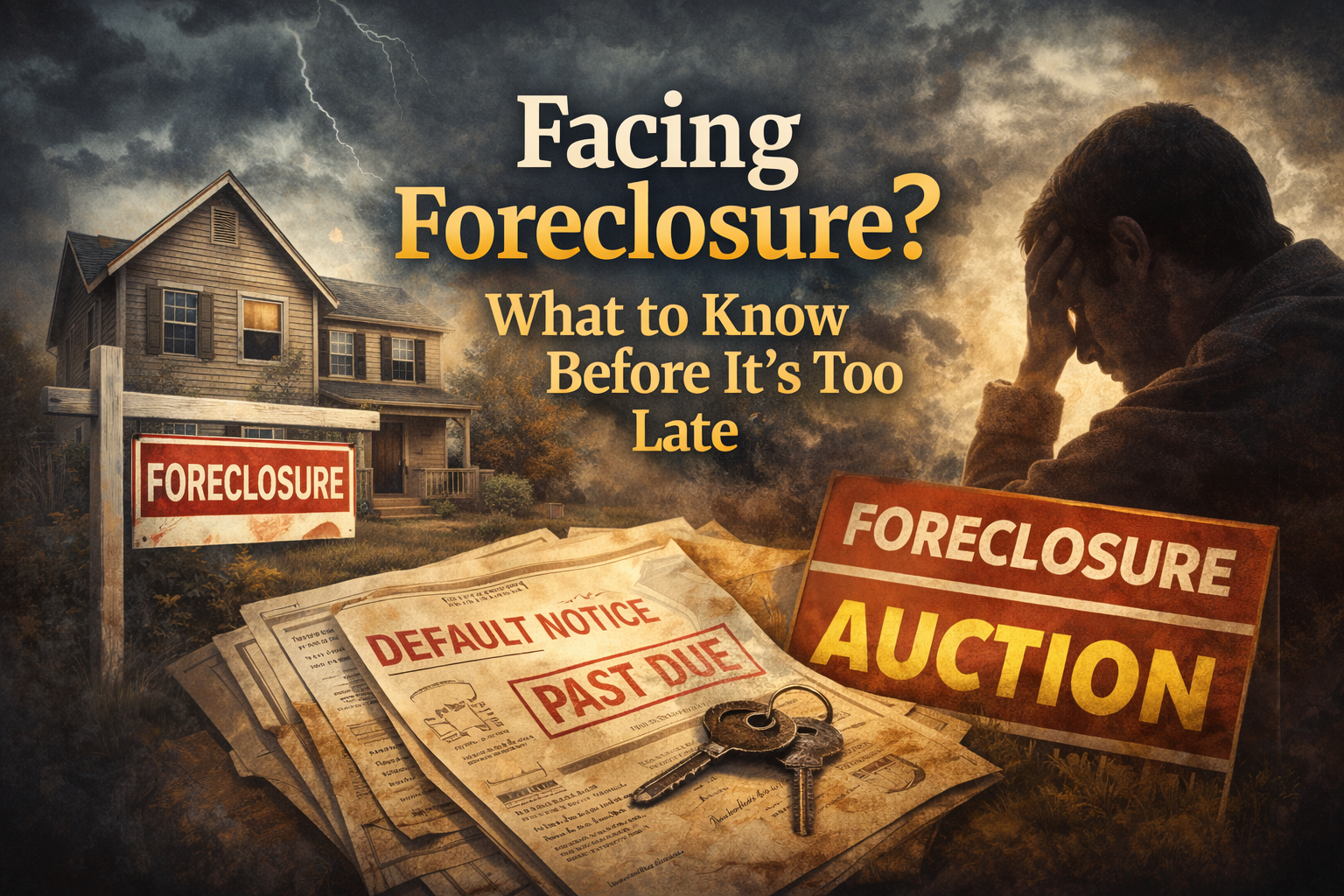

Receiving a foreclosure notice is one of the most frightening experiences a homeowner can go through. The clock starts ticking, the pressure builds, and most people have no idea what their actual options are. Banks count on that. They count on you feeling powerless — because a homeowner who doesn’t know their rights is a homeowner who doesn’t fight back.

But here’s what they don’t advertise: you have more options than you think, and the foreclosure process has specific rules that mortgage servicers are required to follow. When they don’t — and many of them don’t — you have legal ground to stand on.

Understanding the Foreclosure Process

Foreclosure doesn’t happen overnight. There is a legal process, and each step of that process comes with rights and timelines that work in your favor if you know how to use them.

First, a lender must provide written notice that your loan is in default. From that point, there is typically a reinstatement period during which you can bring the loan current and stop the process entirely. If the foreclosure proceeds, most states require a judicial or non-judicial process that takes months — sometimes over a year — before a sale can actually happen.

The key is knowing those timelines and using every available tool to force accountability from your servicer before time runs out.

What Is a Qualified Written Request — and Why It Matters

One of the most powerful tools available to a homeowner facing foreclosure is the Qualified Written Request, or QWR. Under federal law, a QWR forces your mortgage servicer to respond in writing with a complete accounting of your loan — payment history, fees charged, escrow statements, and more.

Why does this matter? Because servicers routinely make errors. Misapplied payments, unauthorized fees, and improper escrow calculations are more common than most people realize. A properly drafted QWR puts them on the legal clock — they must respond within specific timeframes or face penalties. It also creates a paper trail that documents their compliance — or lack of it.

At A.W.A.R.E, our Powerful Qualified Written Request Done For You service handles this entire process on your behalf. We build the document, you send it. And what comes back in response often changes the entire dynamic of your foreclosure situation.

Your Options Before a Sale

If you are in the foreclosure process right now, here are the options most homeowners are never told about:

Loan Modification — You can formally request a modification of your loan terms. Servicers are required to review this request before proceeding with a sale in many circumstances.

Administrative Process — Using proper administrative procedures, you can formally dispute the debt, demand validation, and create a legal record that puts the burden of proof on the lender.

Bankruptcy — Filing for Chapter 7 or Chapter 13 bankruptcy triggers an automatic stay, which immediately pauses foreclosure proceedings. This is a legitimate legal tool — not a last resort.

Done For You Foreclosure Relief — A.W.A.R.E offers both a DIY process package and a full done-for-you service where our team builds everything you need to file and fight back.

Don’t Wait Until the Sale Date

The most common mistake homeowners make is waiting too long. Every day that passes in foreclosure is a day you are not using the tools available to you. The earlier you take action, the more options remain open.

If you are facing foreclosure or have received a notice of default, reach out to the team at A.W.A.R.E today. Visit AreWeAllReallyEducated.com to explore our foreclosure relief packages and take control of your situation before time runs out.

The CFPB outlines foreclosure protections and timelines that every homeowner should understand before taking action.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment